Smart Grids & Energy Data: Africa’s Untapped VC Goldmine

Introduction

The Silent Software Opportunity in Africa’s Clean Energy Push

Africa’s energy transition has entered its infrastructure decade. Across the continent, billions are being invested in solar farms, minigrids, transmission networks, and electric mobility. Yet beneath this visible layer lies an invisible one: the data infrastructure that coordinates generation, storage, and consumption.

In mature markets such as the United Kingdom, where I’m primarily based, this invisible layer, composed of software, APIs & analytics platforms, has driven outsized value creation. The most disruptive energy players, from Octopus Energy’s Kraken to OVO’s Kaluza, have proven that software, not steel, unlocks system-wide efficiency and venture-scale returns.

In contrast, Africa’s power systems remain digitally fragmented. Most utilities lack real-time visibility. Energy data is siloed across Original Equipment Manufacturers (OEMs), operators, and financiers. Yet this fragmentation represents not a weakness, but an opportunity: a chance to leapfrog towards a digital-first energy ecosystem where flexibility, data-driven finance, and grid intelligence become investable frontiers.

In this article, which is a follow-up of my previous article What Is VC-able in Africa’s Renewable Energy Space Today?, I argue that smart grid software and energy data platforms will define the next wave of venture-scale growth in African clean energy. The continent’s decentralised grids and mobile-first economies create the ideal conditions for API-first, asset-light innovation.

Drawing on my extensive knowledge of developing projects across Africa, and my experience in the United Kingdom and case studies from its digital grid revolution, I outline the strategic parallels and offer an investment framework for founders and funds ready to build, or back, the “brains” of Africa’s energy future.

I. The Hidden Infrastructure of Energy: Data as the New Value Layer

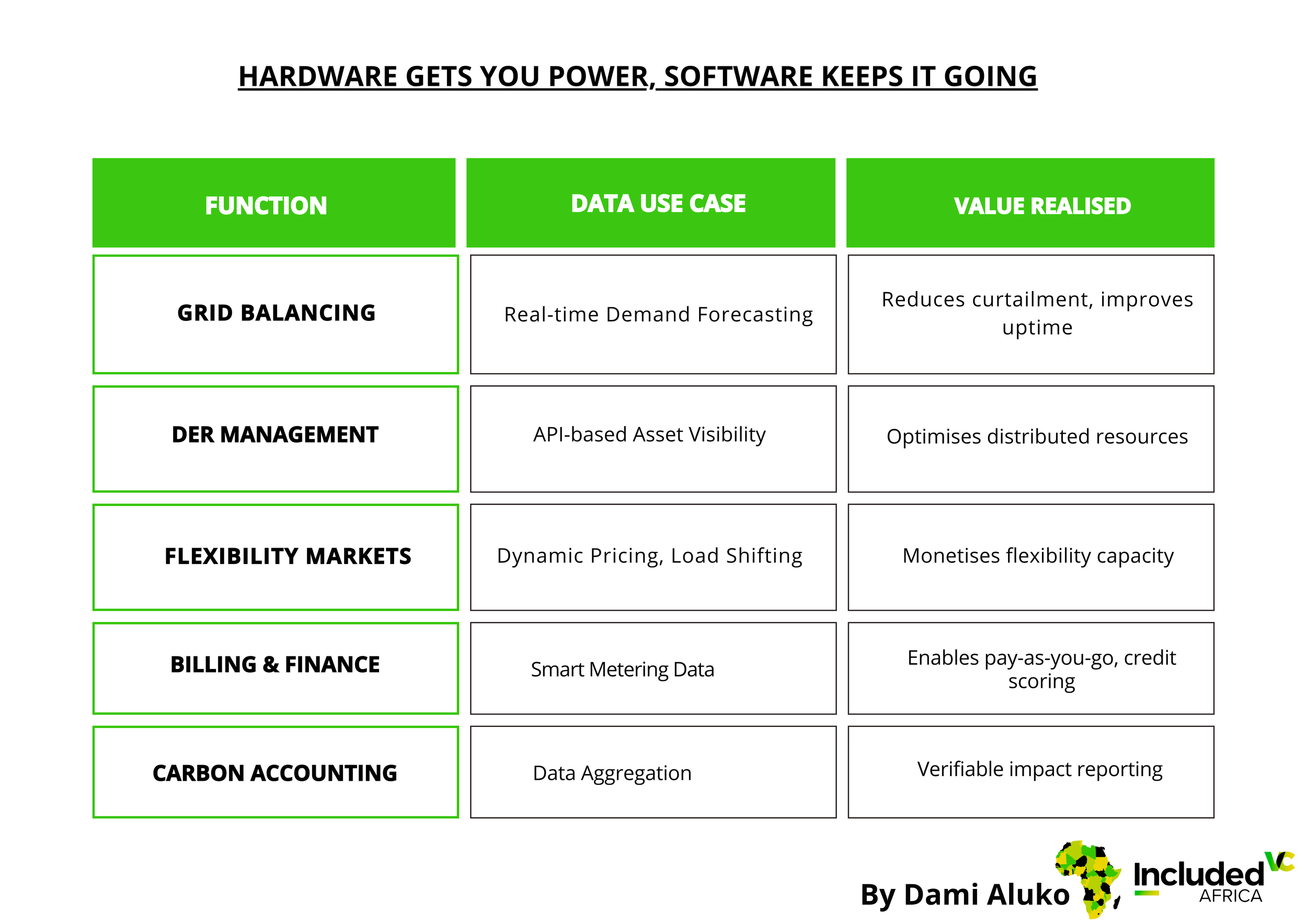

Hardware Gets You Power; Software Keeps It Flowing

African energy investment still overwhelmingly flows into hardware: solar panels, minigrids, EV chargers, and transmission lines, a tale I’m very familiar with. These are essential for capacity expansion but insufficient for system reliability. Think of it this way: hardware delivers megawatts; software delivers intelligence. You might remember from my previous article that my very first foray into the energy industry (2016–2018) was at a smart metering and analytics company in Nigeria, working in the research and development department.

In digital energy systems, data is the infrastructure. It enables forecasting, demand-response, flexibility trading, and asset optimisation, all critical to maximising return on deployed capital. You might wonder if my experience of the considerably more advanced UK energy sector is making me think too far ahead of the African energy context, but no, I’m not. We need to infuse this into the African context as we install solar panels and lay transmission lines. Consider the data layer as the catalyst to scale Africa’s power systems.

The United Kingdom’s National Grid Energy System Operator ESO estimates that flexibility and balancing markets enabled by digital data layers now represent £2–3 bn in annual system value. None of that would exist without interoperable data.

TL;DR: In digital energy, the “pipes” (hardware) are low-margin and capital-heavy. The “protocols” (software) generate recurring, scalable, high-margin value. Again, you might recognise this view from my previous article on “What’s VC-Able in Africa’s Renewable Energy Space?”

II. Africa’s Data Blind Spot: A Problem Worth Solving

Despite rapid growth in solar, batteries and mini-grids, Africa faces three structural data challenges:

Visibility Gap & Revenue Leakage

Many utilities in Sub-Saharan Africa suffer significant non-technical losses. Studies show that in some systems, 20–40% of the electricity distributed is not billed or collected. For example, in Uganda, the utility Umeme reported a ~19% loss in a previous period. When utilities lack real-time data or interoperable metering, they struggle to stabilise business models, making investment riskier. Software platforms that provide meter-to-cloud visibility can reduce that risk, improving creditworthiness and unlocking capital.

Asset & Grid Data Blind-Spots

On the generation and asset side: solar farms, battery systems, mini-grids, many projects lack standardised telemetry, remote diagnostics, degradation modelling or interoperability. Without this data, asset operators cannot optimise operations, and financiers remain cautious. The absence of a data layer becomes a barrier to both performance scaling and investment readiness.

Fragmentation & Siloed Development

Africa’s energy sector has multiple siloes: off-grid companies, mini-grid players, rooftop developers, utilities, regulators, etc., each of which often deploys its own hardware and software stack. The result: fragmented data, poor interoperability, and no unified asset-orchestration layer. But each of these siloes also represents an addressable market for software-first entrants who can standardise data flows, integrate systems, expose APIs and aggregate value across the stack.

Yet fragmentation breeds opportunity. The startup that solves data aggregation and standardisation becomes the data infrastructure provider — the operating system connecting utilities, developers, and financiers.

Case Illustration:

In Uganda, Umeme’s limited data granularity means voltage drops and outages often go undiagnosed for days.

In Nigeria, developers rely on manual consumption logs to design C&I solar systems, a tale I’m very familiar with. I’ve probably “data-logged” up to 65 C&I clients across Africa.

A data-layer startup providing an API bridge across these fragmented endpoints can become indispensable infrastructure.

TL;DR: Africa’s “energy data void” is the equivalent of pre-fintech Africa before API-led innovations like Flutterwave or Paystack. The first movers to build energy data rails could achieve similar platform dominance.

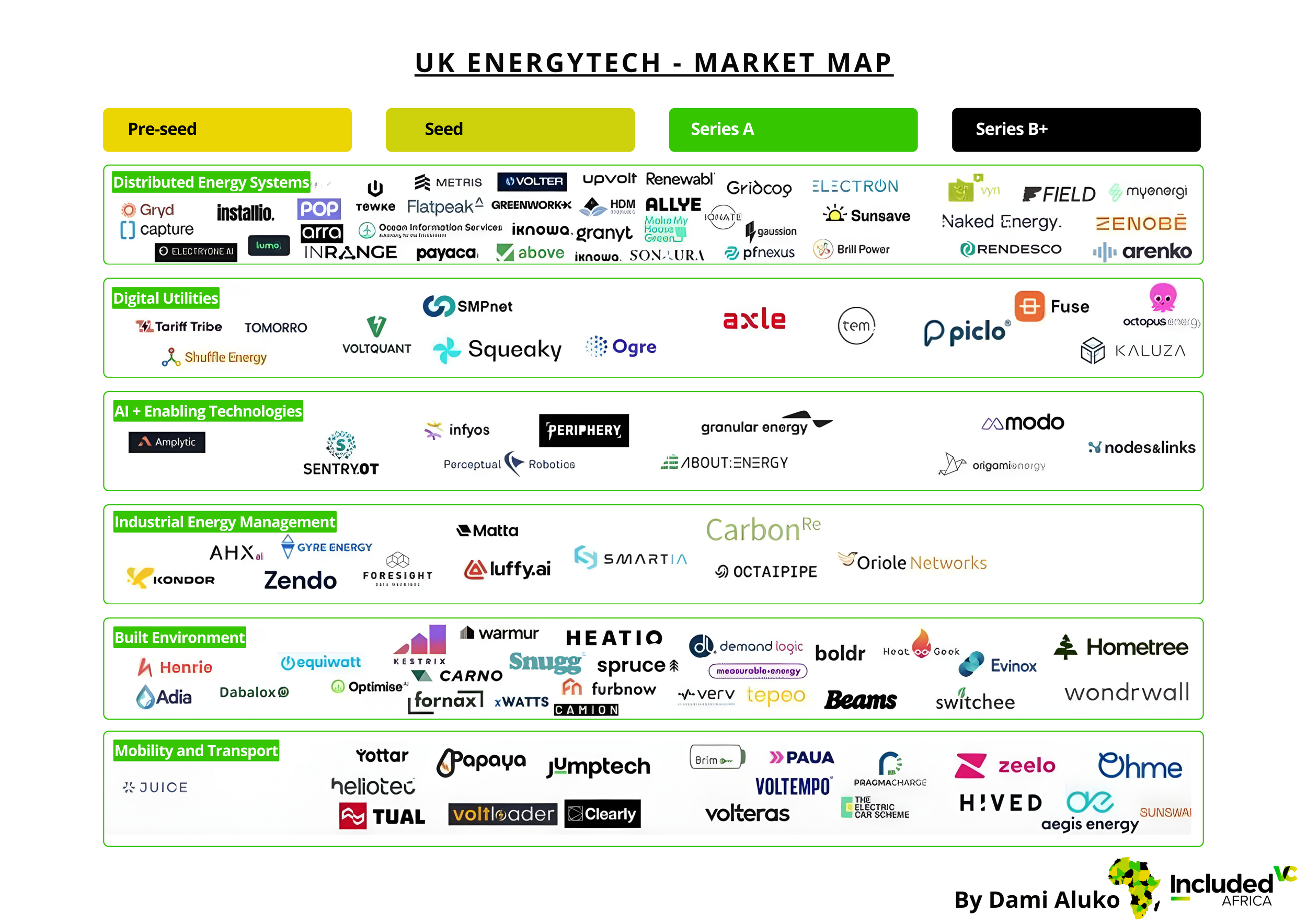

III. Learning from the UK: The Digital Grid Revolution

The UK as a Global Benchmark

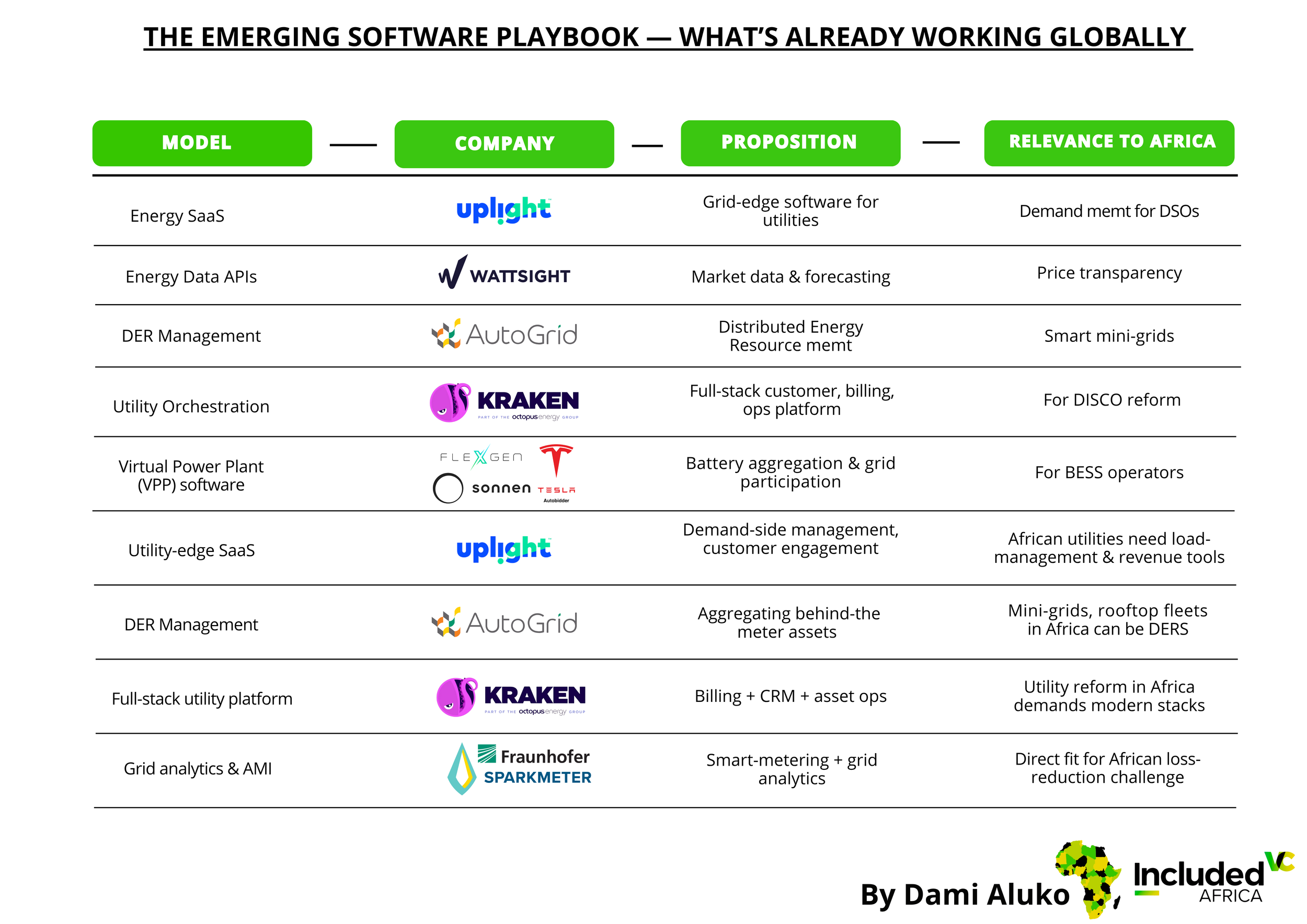

#In the UK, I have experienced how companies evolve from hardware or utility tools into full-stack software platforms. For example:

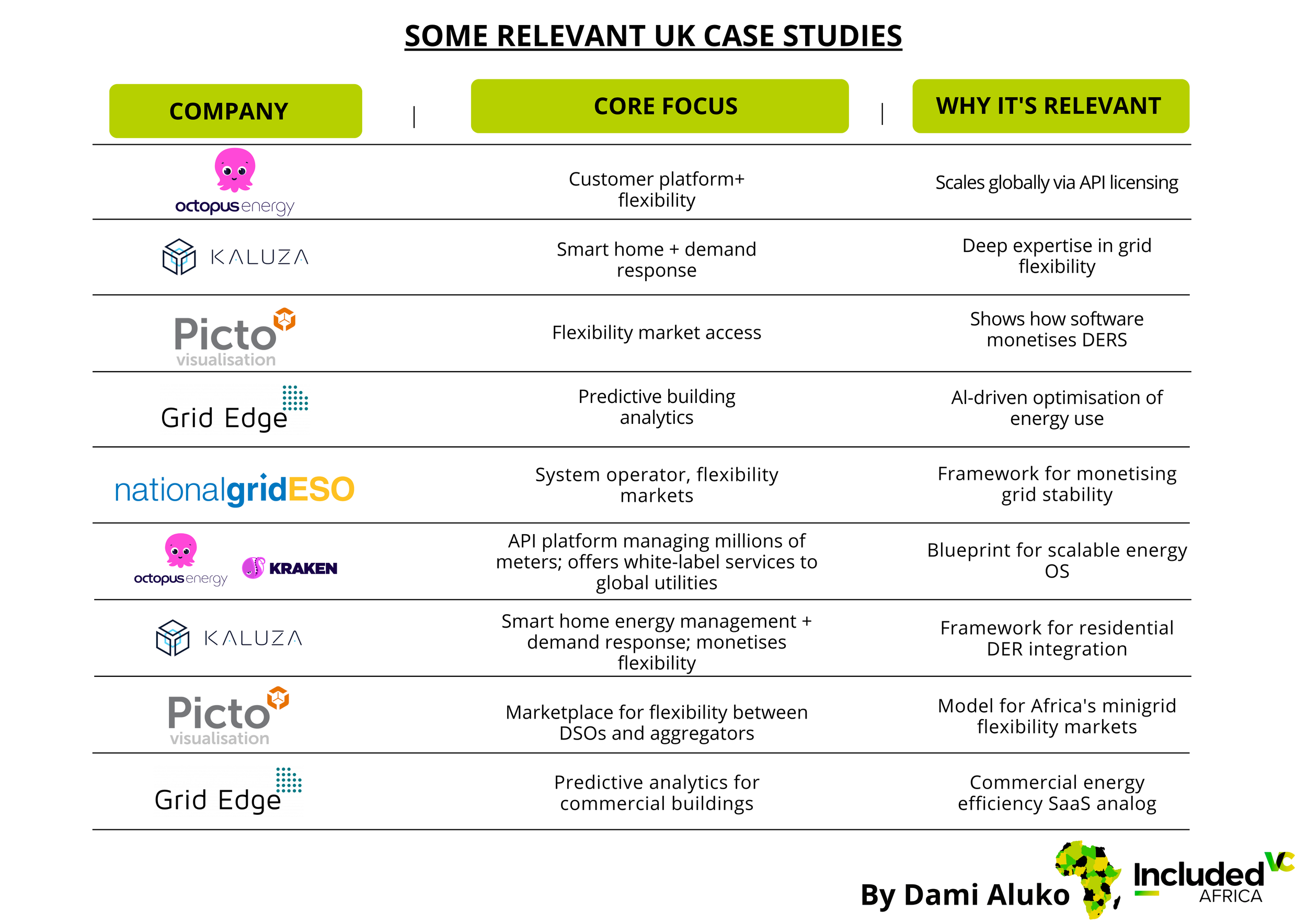

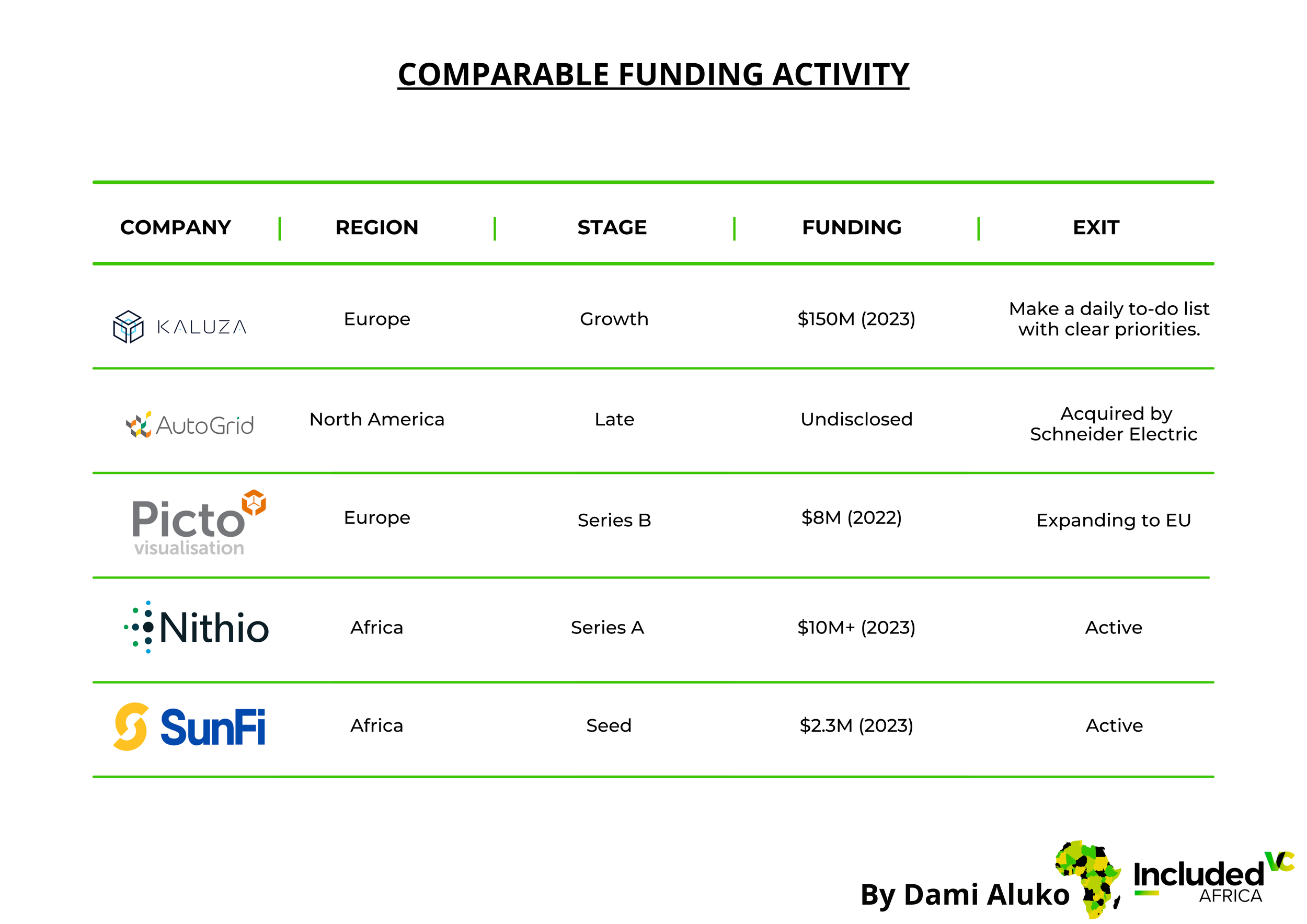

Octopus Energy’s Kraken platform began as the company’s internal customer and asset-management system, but through API licensing and white-label offerings, it has become a global software business.

Kaluza, spun out from OVO, provides home-energy management, demand response and flexibility orchestration. Its software is region-agnostic and built for scalability.

Grid Edge (UK) uses AI to optimise commercial building energy consumption and asset performance, showing how analytics can create value in the built environment.

Piclo Flex acts as a digital marketplace for grid flexibility, connecting DSOs to aggregators.

The pattern is clear: SaaS-first, API-enabled software becomes the hub of value. These companies grew by converting the data generated by existing energy hardware and networks into high-margin services.

In my UK-based work, I have witnessed the barriers and enablers of that transition: injecting analytics into smart grids, integrating BESS into dispatch models, and connecting EV-charging infrastructure data to utility platforms. These lessons are directly relevant to Africa. For example, a mini-grid operator in Nigeria could mirror UK flexibility markets by using data from its fleet of assets to sell services to a local Distribution System Operator, known as Distribution Company (DisCo) in Nigeria.

If an African startup builds data infrastructure with the same architectural philosophy: modular, cloud-native, API-first, it can replicate across countries faster because the hardware base (solar panels, batteries, meters) is already being deployed. The software layer is the arbitrage.

Translating the Model for Africa

Africa’s energy systems, decentralised, mobile-first, and often unbundled, are actually more digitally “leapfroggable” than Europe’s.

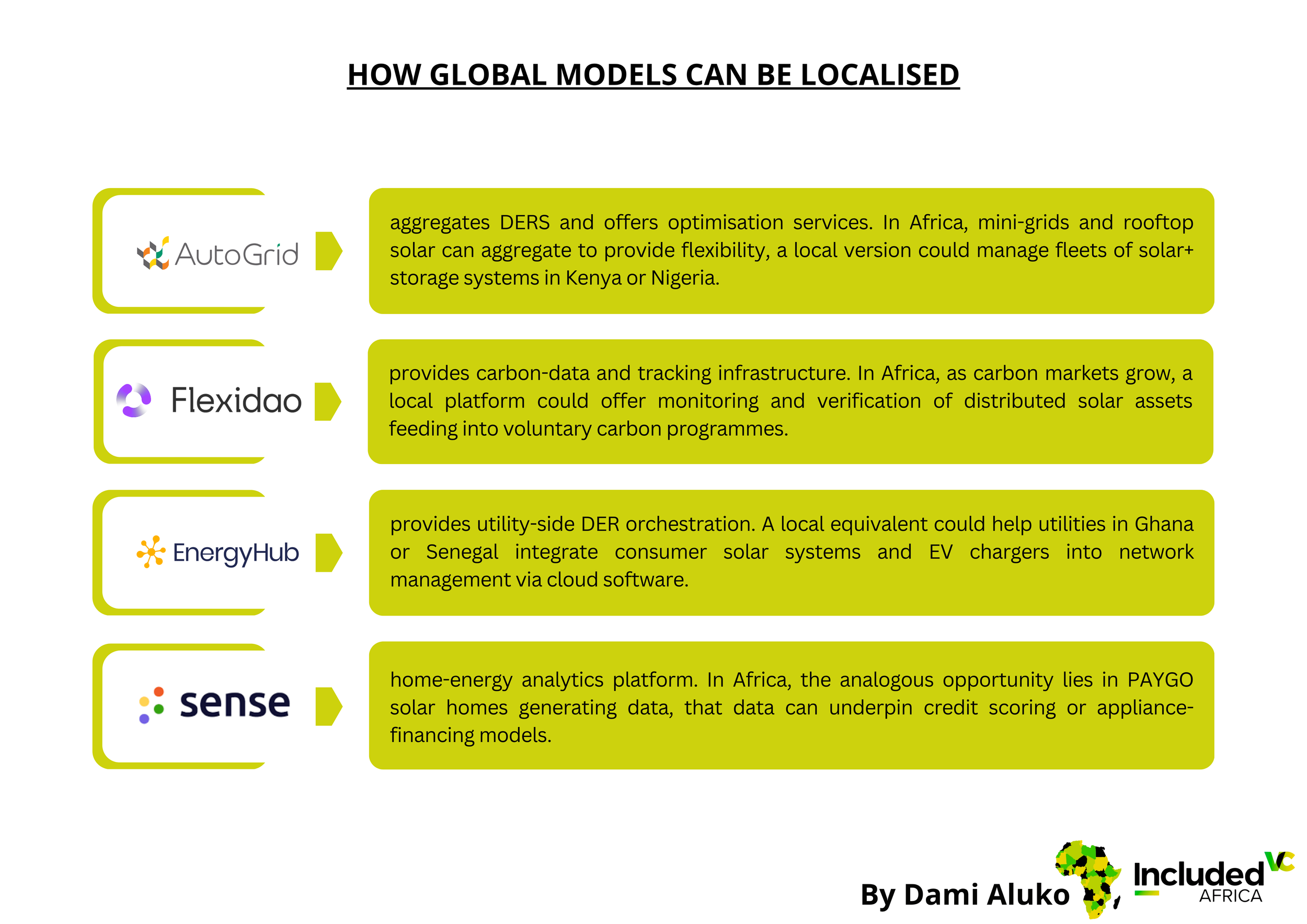

Octopus’ Kraken could inspire API-licensed platforms for African solar aggregators to manage DER fleets.

Kaluza’s demand-response model could underpin C&I solar load optimisation in Kenya or Ghana.

Piclo’s flexibility marketplace could be adapted to minigrid-level balancing, allowing Distribution System Operators to contract flexible demand from clusters of solar homes or cold-storage operators.

Each model, stripped of heavy hardware assumptions, becomes an opportunity for African founders and investors to export software.

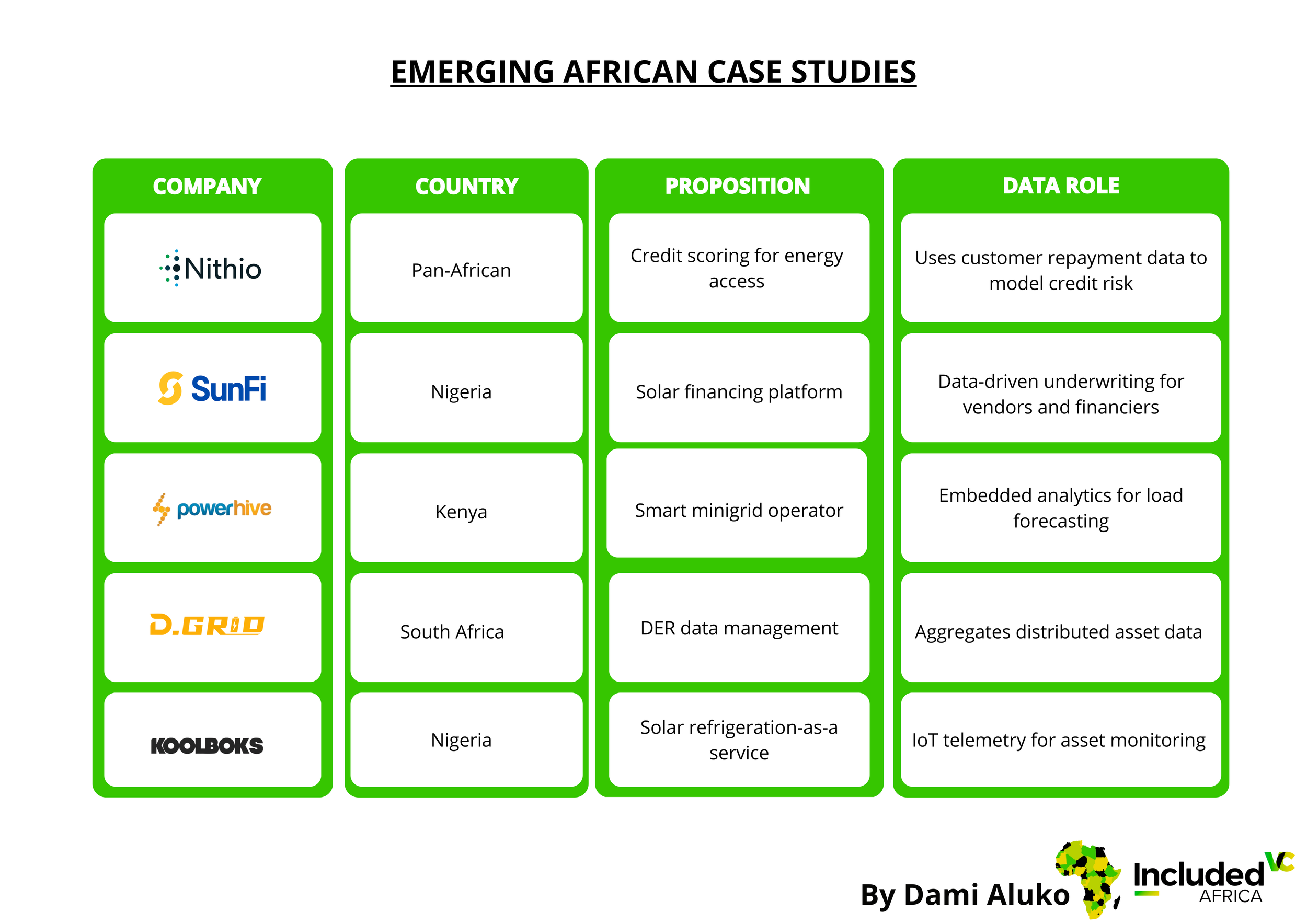

IV. Emerging African Case Studies: Data-Driven Energy Innovation

While nascent, Africa’s digital energy startups are already demonstrating the power of data-centric models. While the software layer in Africa remains thin, several early movers are already signalling what is possible. These are not pure hardware vendors; they are data companies in disguise.

Powerhive (Kenya): Embedded metering and analytics on its mini-grid systems to understand demand patterns, optimise operations and monetise connectivity.

Nithio (Pan-Africa): Uses geospatial, credit-behaviour and energy-consumption data to underwrite receivables-backed solar finance. In Nigeria, it acts as the monitoring-agent for an $80mn facility.

SunFi (Nigeria): Provides a SaaS platform connecting solar vendors, financiers and asset-operators, enabling data-driven underwriting, tracking and performance insights.

DGrid (South Africa): Manages distributed generation asset data platforms for C&I clients, enabling performance monitoring and optimisation.

Koolboks (Nigeria): While primarily an appliance-as-a-service company, it collects IoT telemetry from its solar fridges, providing data streams that value financiers and asset managers.

These companies aren’t utilities. They are data companies disguised as energy providers. Each is creating a feedback loop of data → insight → capital → deployment, improving financing efficiency and asset performance.

TL;DR: The common pattern is “data as risk mitigator.” In fragmented markets, where energy project risk is high, startups that quantify and de-risk through analytics attract investor confidence faster.

V. How Global Models Can Be Localised

Global data-energy software models provide useful frameworks, but localisation is critical for Africa. Let’s examine how global analogues can be adapted.

Global Analogues and Lessons

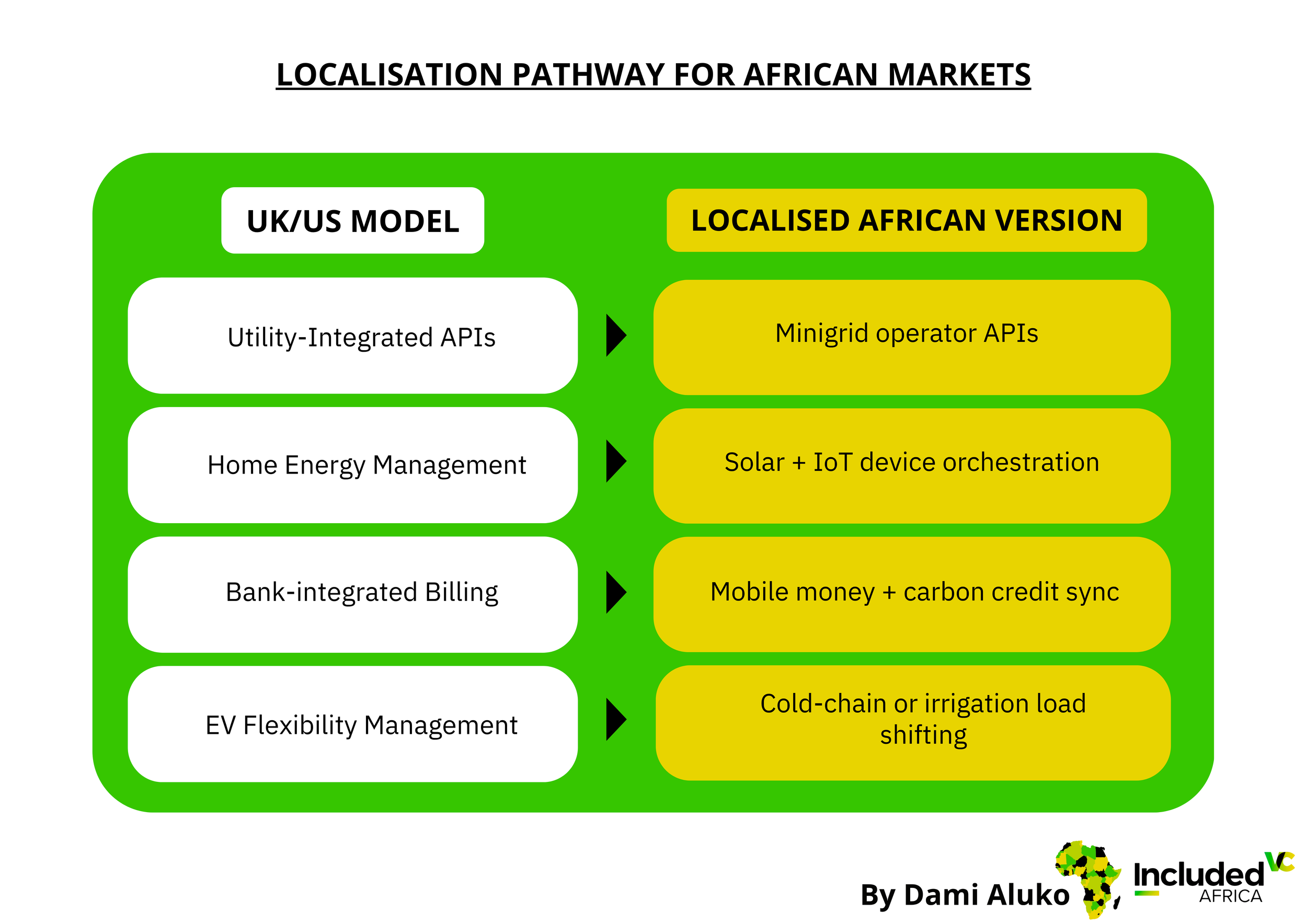

Africa’s advantage lies in mobile-native infrastructure and leapfrogging legacy systems. A UK startup may retrofit smart meters; an African startup designs around them.

Localisation framework

Replace hardware dependency with IoT + mobile-first monitoring, because mobile penetration in Africa is high and mobile infrastructure is often more reliable than grid infrastructure.

Design API-first architecture from day one — expose endpoints for inverters, meters, mobile money payments, and carbon registries.

Integrate with mobile money & carbon registries to enable monetisation beyond pure energy — e.g., payments, carbon credits, trading.

Treat the software business as the “Energy OS for Africa” — a modular layer connecting utilities, mini-grids, solar developers, financiers, and end users.

Africa does not need to replicate Western models; it can adapt them for its realities.

VI. Building API-First Energy Startups in Africa

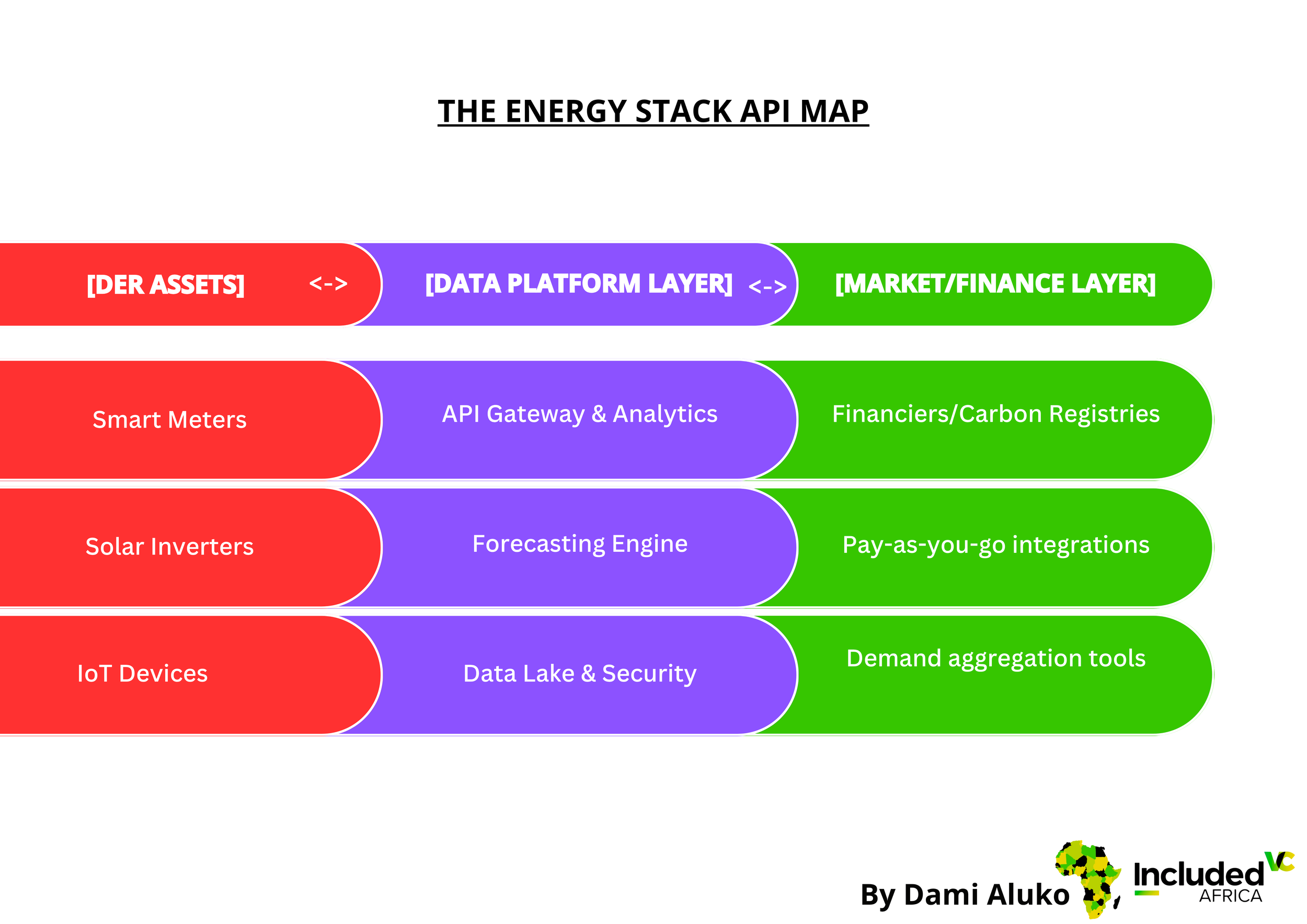

What “API-First” Means

An API-first energy company builds for interoperability from day one. It creates the connective tissue that allows other players to plug into data, billing, or asset control seamlessly.

Core Principles:

Modular design with clear endpoints (meter, tariff, asset, customer).

Secure data standardisation (open energy schema).

Scalable pricing models (usage-based or per-asset fees).

Integration-ready architecture (for fintech, carbon, or insurance partners).

Practical steps for founders:

Define core data model — asset, user, meter reading, tariff, kWh, event timestamp.

Expose endpoints — /meter-reading, /asset-status, /tariff-history, /energy-forecast.

Offer developer-friendly documentation — e.g., Swagger-UI, sandbox APIs enabling third-party integrations.

Launch with a niche use-case — for example, asset-health monitoring for solar farms or inverter monitoring for mini-grids.

Monetise via SaaS/API usage — for example, £/asset/month or US$/kWh-data-point, or via licensing to utilities.

Scale horizontally — once you gather enough assets in one market, you can replicate to another country with minimal incremental hardware.

The beauty of this model is that you unlock software economics — low marginal cost, high replication, licensing potential, and even exit potential via acquisition by global platforms or utilities.

VII. Investor Lens: Why This Is Venture-Backable

The Business Case

Smart grid and energy data startups are:

Asset-light — low capex, scalable through software distribution.

Recurring-revenue models — subscription, API call, or transaction fees.

High gross margins — typical SaaS margins exceed 70%.

Technology moat — data aggregation, analytics, platform effects.

The Market Opportunity

The global energy analytics market is projected to surpass $10 billion by 2030, growing at ~15% CAGR.

Africa currently represents less than 1% of this value, a massive whitespace.

By 2030, sub-Saharan Africa’s distributed energy assets could exceed 40 million units (solar, batteries, IoT devices), all data-producing endpoints.

TL;DR: Africa’s “energy intelligence” sector today looks like Europe’s 2015 clean-tech data scene — pre-consolidation, pre-institutional capital, but with exponential upside for early entrants.

Exit Pathways

Strategic M&A: Global utilities, infrastructure funds, and software firms are actively acquiring digital grid capabilities.

Private equity roll-ups: Data platforms aggregating assets across African markets could attract regional consolidation plays.

Public listings: As regulatory frameworks mature, API-led energy firms could become sustainability tech flagships.

For African investors, the chance is to get in early on the software layer rather than battle hardware cost curves. For VCs, the arbitrage is clear: invest in data, not just iron.

VIII. Policy and Ecosystem Enablers

For Africa’s digital grid ecosystem to flourish, enabling conditions must evolve:

Open Data Regulation: Encourage sharing of non-sensitive grid data to allow third-party innovation.

Regulatory Sandboxes: Governments should emulate the UK’s Ofgem model, allowing pilots of flexibility and demand-response schemes.

DFI and Donor Catalysts: Multilateral agencies can fund data infrastructure as a public good, similar to broadband investments.

Talent and Technical Capacity: Upskilling developers to understand both data science and energy systems is key.

IX. The Call to Action — Building the Brain of Africa’s Energy Future

Africa’s energy transition is no longer solely about building wires, it’s also about building intelligence. The continent will add hundreds of millions of new energy connections this decade, each producing data that can unlock new markets and efficiencies.

The question is not whether Africa will digitise its grid; it’s who will own the software layer that coordinates it.

For Founders:

Start API-first, not hardware-first.

Build interoperable platforms for DER management, billing, or carbon integration.

Monetise insights, not installations.

For Investors:

Treat digital energy as a “picks and shovels” play — essential infrastructure for the clean energy gold rush.

Back founders who combine energy expertise + data fluency.

Take a patient but conviction-led approach; the compounding value of energy data is exponential.

For Policymakers:

Open the gates for innovation by releasing grid data and enabling pilot programs.

Prioritise interoperability standards across national and regional grids.

Having worked within the UK’s digitally mature grid ecosystem, I’ve seen how data unlocks capital, optimises energy use, and fuels innovation. Africa now stands on the brink of that same transformation — one that could yield not just reliable power, but a new generation of globally investable technology ventures.

Conclusion

Hardware powers electrons; software powers intelligence.

In the next decade, Africa’s clean energy leapfrog will depend not on who builds the panels or grids, but on who builds the data rails and software brains to connect them.

The continent’s next unicorns may not own a single megawatt, but they’ll orchestrate millions.

Dami Aluko works at the intersection of clean energy, data, investment & technology. Primarily based in the United Kingdom, I help organisations design smarter grids, scale distributed energy, and unlock climate-tech opportunities. My 10-year industry background spans C&I solar, demand-side response innovation, minigrid systems, technical–commercial modelling, smart grid strategy, energy data analytics and project finance for clean energy infrastructure.

If you’re keen to have a chat about anything I’ve written, feel free to reach me directly at: damilarealuko@gmail.com.

Let’s build a cleaner future for the planet, together!